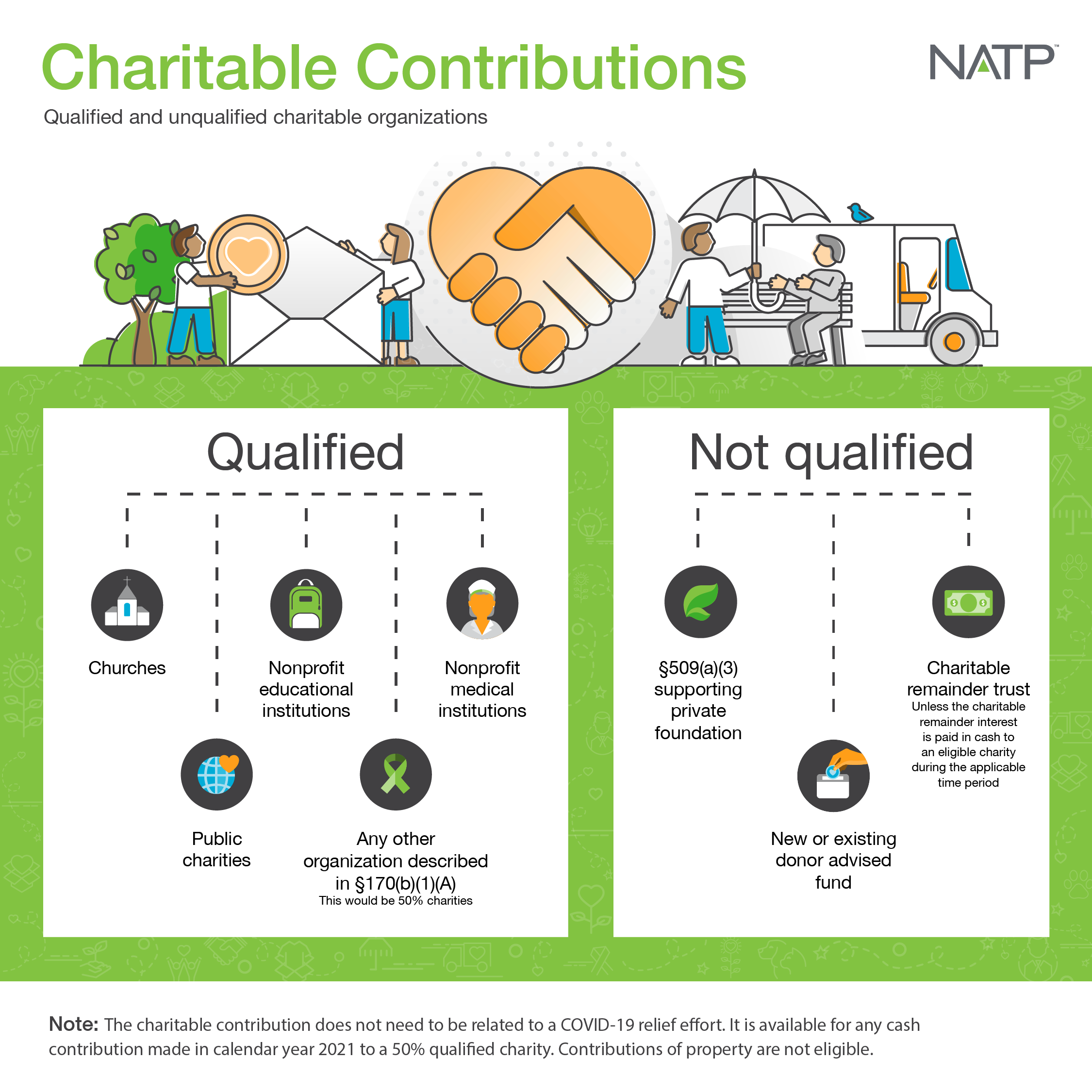

A recent memo issued by the IRS Chief Counsel’s Office makes it clear that the agency will reject claimed deductions for a non-cash donation to a charitable organization if there was no clear intent on the part of the taxpayer to donate the property. The memo (20233201F), stated that a taxpayer could not claim a deduction for the difference between the fair market value (FMV) of a property and the amount the taxpayer received in a bargain sale to an unnamed qualified nonprofit organization.

Field attorney advice memorandums issued by the Office of Chief Counsel can’t be relied upon by taxpayers as precedent, but they do lay out the agency’s position on an issue and the reasoning behind it. In the case of the taxpayer who was attempting to deduct the difference between the FMV of a property and the amount received in a bargain sale to a charitable organization, the IRS found there was no intent to make a gift and nothing of value to donate after the property was sold.

The memo is heavily redacted, so it is impossible to know who the parties to the transaction were, the amounts at issue and when the events described took place. Thus, the descriptions of the taxpayer’s situation are only outlined in general terms. While not specifically stated in the memorandum, it seems likely the taxpayer was trying to claim a donation to the local governmental unit where the property was located.

Sale price agreed upon to end litigation

The charitable organization made an offer to purchase property owned by the taxpayer that was accompanied by a substantial payment. However, after multiple appraisals conducted by the taxpayer and the organization, they could not agree on a purchase price.

The taxpayer then documented their intent to decline the organization’s offer and sell to another party, and the matter ended up in court. The case was resolved by a stipulation that stated the parties could not agree on the property’s FMV, but that the taxpayer was selling it to the organization for the amount it initially offered. A stipulation is a written agreement between parties that resolves all of the matters addressed in the document.

The taxpayer’s returns claimed a deduction for a charitable contribution as a result of the bargain sale of the property to the charitable organization. The amount of the deduction was the difference between the property’s appraised value and the sale price.

Attempted third-party sale shows no charitable intent

The Office of Chief Counsel determined that the taxpayer’s intent to sell the property to a third party for a higher amount than was offered by the charitable organization and their failure to accept the organization’s lower offer indicates that the taxpayer did not intend to make a gift. The taxpayer accepted the organization’s lower offer as a stipulation to settle litigation. After the parties signed the stipulation, the taxpayer lacked any rights in the property at issue, so it could no longer attribute any value to the property in excess of what was paid.

The memo also noted that the taxpayer did not properly substantiate the claimed deduction because they did not prove its FMV. While the charitable organization provided a Form 8283, Donee Acknowledgement, for the property, it did not provide an FMV for the property and never stated that the property had value in excess of the sale price.