Charitable contributions are a great way to support organizations you care about and your local community! On top of that, depending on your client’s tax situation, donations to a qualified charitable organization could be a way for them to reduce their tax liability at the end of the year.

The Taxpayer Certainty and Disaster Relief Act of 2020 (TCDRTA) provided more tax incentives for individuals and corporations making charitable contributions on 2021 returns. It extended the suspension of the adjusted gross income (AGI) percentage limitations on the deduction of cash contributions by individuals for qualified charitable contributions. It also allows a deduction of up to $300 ($600 for married filing jointly filers) for non-itemizers for tax year 2021.

For 2021, the charitable deduction is claimed as a deduction in calculating taxable income (as opposed to an above-the-line deduction in calculating AGI for 2020).

Individual contributions

Generally speaking, only individual taxpayers who itemize their deductions qualify for a charitable contribution deduction. The itemized deduction for charitable contributions is limited to a percentage of the taxpayer’s AGI, computed without regard to the charitable deduction and any net operating loss (NOL) carrybacks.

The type of organization receiving the donation and property donated determines the percentage. For tax years beginning after Dec. 31, 2017, and before Jan. 1, 2026, the contribution base for cash contributions by individuals to 50-percent public charities increased from 50% to 60% of AGI.

The TCDTRA suspended the 60% limitation on the deduction of charitable cash contributions for 2021. The cash contribution must be made after Dec. 31, 2020, and before Jan. 1, 2022, to a qualified charity to qualify for the 100% deduction.

An individual may claim an itemized deduction for contributions to a charitable organization on Schedule A (Form 1040).

Qualified charitable organizations

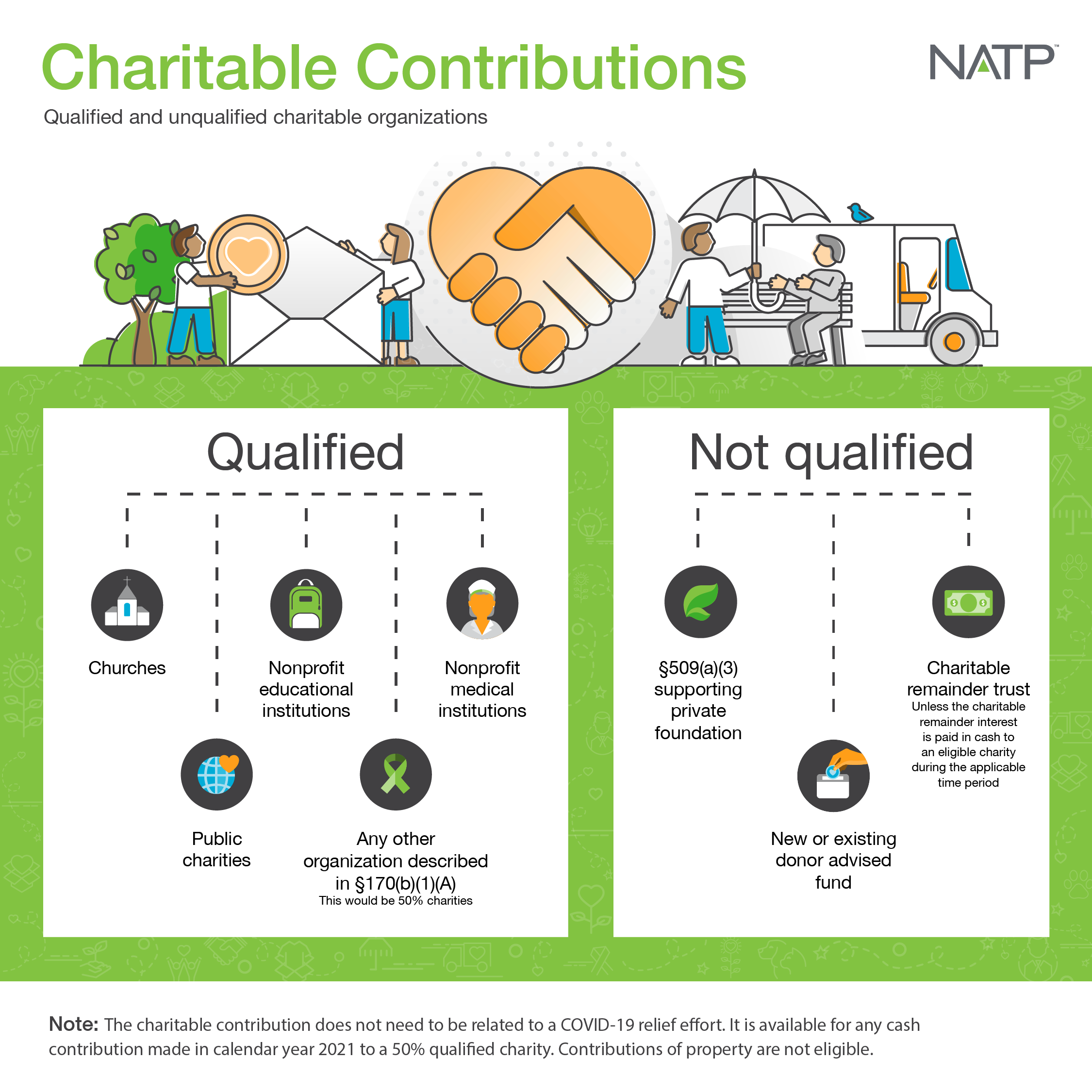

The following organizations are considered qualified charitable organizations:

- Churches

- Nonprofit educational institutions

- Nonprofit medical institutions

- Public charities

- Any other organization described in §170(b)(1)(A)

- This would be 50% charities

The following organizations are not considered qualified charitable organizations:

- §509(a)(3) supporting private foundations

- New or existing donor advised funds

- Charitable remainder trusts, unless the charitable remainder interest is paid in cash to an eligible charity during the applicable time period

The definition of qualified charity is also the same one used by a corporation when looking at qualifying corporate donations.

More information

There are of course many more steps tax preparers need to be aware of to complete a 2021 return with a charitable contribution, either for a corporation or individual.

More information on this topic was included in NATP’s 2021 Tax Season Update sessions and printed textbook or e-book. The 2022 in-person Tax Season Updates workshops details will be available soon.

The 2021 Virtual Tax Season Updates workshop is still available for free, on-demand, to NATP Premium level members.

About National Association of Tax Professionals

About National Association of Tax ProfessionalsThe National Association of Tax Professionals (NATP) is the largest association dedicated to equipping tax professionals with the resources, connections and education they need to provide the highest level of service to their clients. NATP is comprised of over 23,000 leading tax professionals who believe in a superior standard of ethics and exemplify professional excellence. Members rely on NATP to deliver professional connections, content expertise and advocacy that provides them with the support they need to best serve their clients. The organization welcomes all tax professionals in their quest to continually meet the needs of the public, no matter where they are in their careers.

The NATP headquarters is located in Appleton, WI. To learn more, visit www.natptax.com.

Information included in this article is accurate as of the publish date. This post is not reflective of tax law changes or IRS guidance that may have occurred after the date of publishing.