Given the uncertainty surrounding the pandemic and economic hardships faced by many, we are highlighting two recent court cases many practitioners can relate to and can serve as a cautionary tale of what NOT to do.

Officer compensation in an S-corp

Lateesa Ward v. Commissioner involves an attorney, her law firm (an S corporation), amounts paid for officer compensation, insolvency and travel expense substantiation.

Case details

Lateesa Ward is a Minneapolis attorney who graduated law school in 1991 with $45,000 in student loan debt. Eventually, this debt grew to an amount exceeding $200,000.

She started her career at a big law firm but in 2006 decided to go into business for herself and formed Ward & Ward. This firm was taxed as an S corporation where Ward was the sole shareholder. Ward and another attorney were the only employees for tax years 2011-2013 (the years in question).

Ward had a rough start and was struggling financially with roughly $7,000 of debt discharged in 2012 and $11,000 of debt discharged in 2013.

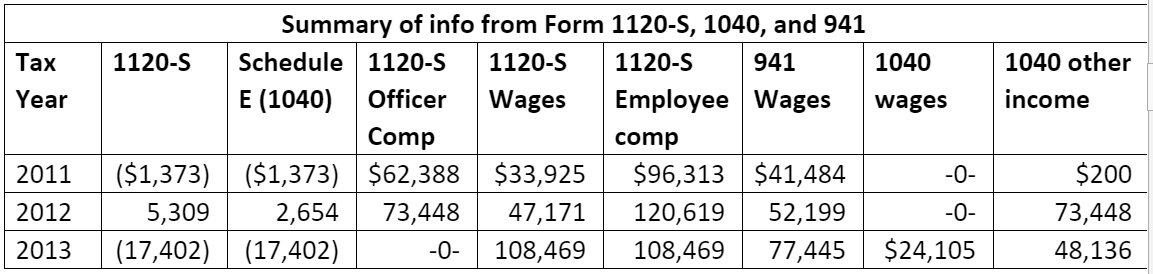

Ward filed the following forms:

- Form 1120-S, U.S. Income Tax Return for an S Corporation

- Form 941, Employer’s Quarterly Federal Tax Return

- Form 1040, U.S. Individual Income Tax Return

- Schedule E, Supplemental Income and Loss

Ward’s S corporation and personal returns were audited, and the IRS found a large number of substantiation problems with officer wages paid from the S corporation, travel expense substantiation, and debt discharge and the insolvency exception.

It should be noted:

- For tax year 2011, the corporation’s income was reported on Schedule E and Schedule C

- The $200 in other income does not appear to be related to the S corporation

- $53,339 (of the $108,469) was paid to the other employee in 2013

- Form 941 wages have been rounded up as cents were included in the form filings

Case outcome

In looking at the summary what jumps out at you as issues on the returns?

If your initial response was something to the effect there is a mismatch on wage reporting, you would be correct.

During all the years in question, the corporation reported compensation and wages that are different from form to form. The wages reported on the corporate return do not match the wages reported on the payroll returns. Also, the wages reported by the shareholder on her personal return do not match what the corporation reported as officer compensation. Also, a deduction for payroll taxes was missing from the corporate return.

Shareholders who perform services receive officer compensation and are considered employees. The employer (corporation) and the employee (shareholder) are subject to unemployment taxes. Social Security and Medicare taxes are withheld from the employee’s compensation and the employer is subject to the tax as well. The employer is liable to withhold the employees’ portion and to submit both portions.

The Commissioner’s position in this case was the employer (firm) did not pay employment taxes on wages Ward received. The firm’s position was some of the compensation paid was wages, but the rest was a distribution of the firm’s earnings and profits.

The firm also said that a portion of the distributions should not be taxed because they were a return of Ward’s basis in the firm. Ward also mentioned her compensation should be taxed to her as self-employment income.

The employer provided no evidence to support the fact that the payments were anything but compensation. A shareholder does not have to include distributions in income if there is basis that exceeds the amount distributed. Distributions are not treated as wages or reported on Form 941. It is the responsibility of the shareholder to maintain basis schedules.

Ward presented no evidence of her basis in the firm for any year. There was no evidence showing Ward’s work for the firm was anything other than as an employee, and no evidence was provided to show these payments were anything other compensation. The Tax Court determined the firm was liable for employment taxes on all amounts the Commissioner identified as officer compensation.

It is unclear from the case, who prepared the returns. If the corporate and personal returns were consistent with the dollar amount of officer compensation, perhaps Ward’s argument that she received compensation and distributions would have been valid if the compensation was reasonable. The distributions would not be taxable, assuming she had basis. The responsibility for the basis schedule is on Ward, not her firm.

Takeaways

One of the takeaways from the case is reconciliation and tie out. The IRS is tying out what is reported on payroll reports, corporate tax returns and individual tax returns.

Basis schedules need to be maintained if tax free distributions are received. As the case mentions, there is some guidance to relieve a firm from employment taxes:

“Section 530 of the Revenue Act of 1978 relieves some firms from liability in situations somewhat like this. A firm that has consistently not treated an individual as an employee isn’t liable for employment tax on compensation paid to that individual unless the firm had no reasonable basis for not treating the individual as an employee.”

The application may be very narrow, but none the less does exist.

Early withdrawals tax

The second case is John Catania v. Commissioner, and at issue is the 10% early withdrawals tax.

Case details

Catania worked for Home Depot and participated in a 401(k) plan. At age 55, he retired in 2014 and transferred his 401(k) to a traditional individual retirement account (IRA).

In 2016 Catania (age 57) withdrew $37,000 from the IRA. The funds were used to pay home maintenance expenses and living expenses. Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance contracts, etc. was received. Catania reported the income on his personal return but did not include the 10% additional tax.

Catania said he qualified for an exception from the 10% additional tax as he was 55 years old when he retired from Home Depot (separated service) and the IRA funds originally came from an employer-sponsored 401(k) plan.

A 10% tax is imposed on the taxable amount of distributions from qualified retirement plans received before age 59 ½ unless an exception to the penalty applies. An exception exists if a distribution is made to an employee after separation from service after reaching age 55 (age 50 for a qualified public safety employee). The exception only applies to certain qualified plans and not to distributions from IRAs.

Case outcome

In looking at the summarized fact pattern, what are your thoughts, is Catania subject to the 10% tax?

If you said yes, Catania is subject to the 10% tax, you would be correct. In reaching the decision, the Tax Court said the funds were transferred from a 401(k) plan to an IRA when Catania retired. The money was withdrawn from an IRA; therefore, the separation from service exception did not apply.

To qualify for the separation of service exception, two conditions need to be met.

The 10% early withdrawals tax does not apply to distributions made to an employee after separation from service after reaching of age 55. A distribution to an employee from a qualified plan is available for this age 55 exception if both of the following conditions are met:

- The distribution is made after the employee has separated from service with the employer maintaining the plan, and

- The separation from service occurs during or after the calendar year in which the employee attains age 55

Takeaways

One has to admit, the argument was creative; although, incorrect. The distribution was made from an IRA, not a qualified plan and that makes a difference.

As mentioned in the opening paragraph, we are still living in uncertain times. Many of our clients are struggling, and as practitioners we are often called on to fix items they did incorrectly and without consulting us.

Because these are court cases, we do not have the intricate details of the taxpayer’s situations. The question we would pose to you would be if these two taxpayers walked into your office today seeking help and the fact pattern was a 2020 fact pattern, what could you do to help the taxpayers?

Many things may come to mind with the first case including amending payroll reports, creating a basis schedule and educating the taxpayer.

In the second case, it would be what are the exceptions to the 10% early distributions tax and would possibly any of the exceptions apply. They may not, but it’s worth asking questions.

If you’re working on a client’s return and have questions about IRA distributions or the additional exceptions, you can call our team of expert tax researchers who answer thousands of questions each year on a variety of federal tax issues affecting your clients.

About National Association of Tax Professionals

About National Association of Tax ProfessionalsThe National Association of Tax Professionals (NATP) is the largest association dedicated to equipping tax professionals with the resources, connections and education they need to provide the highest level of service to their clients. NATP is comprised of over 23,000 leading tax professionals who believe in a superior standard of ethics and exemplify professional excellence. Members rely on NATP to deliver professional connections, content expertise and advocacy that provides them with the support they need to best serve their clients. The organization welcomes all tax professionals in their quest to continually meet the needs of the public, no matter where they are in their careers.

The NATP headquarters is located in Appleton, WI. To learn more, visit www.natptax.com.

Information included in this article is accurate as of the publish date. This post is not reflective of tax law changes or IRS guidance that may have occurred after the date of publishing.